UniCredit Bank Austria Business Indicator:

Economic recovery slow to materialise

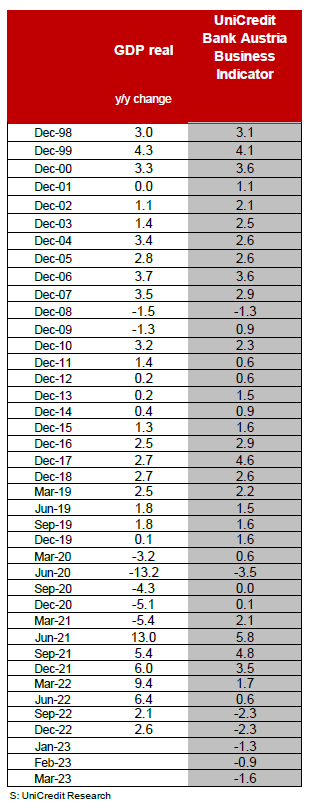

- UniCredit Bank Austria Business Indicator falls to minus 1.6 points in March

- Temporary setback on road to economic recovery due to declining sentiment in parts of services sector and domestic industrial sector

- High inflation delaying recovery but return to limited economic growth likely in Q2

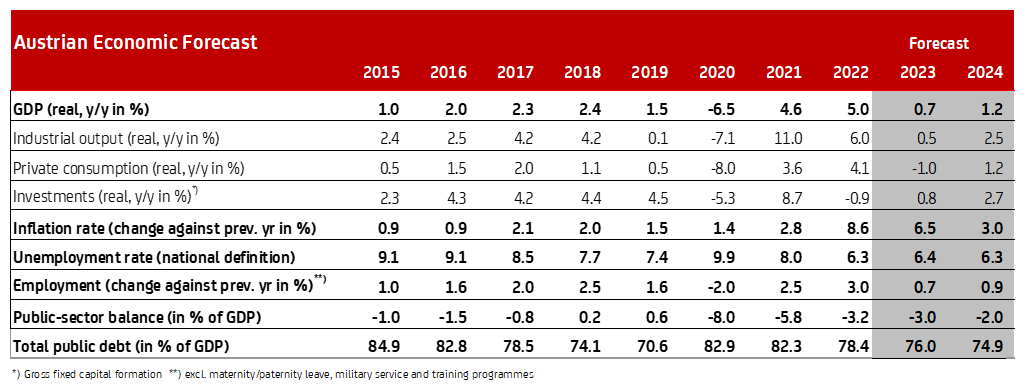

- Moderate economic growth of 0.7% expected for 2023 overall and 1.2% for 2024

- Unemployment rate still forecast to be 6.4% 2023 and 6.3% for 2024

- Services prices slowing inflation climbdown: Inflation in Austria set to noticeably outstrip eurozone at 6.5% for 2023 and 3.0% for 2024

- Cycle of monetary tightening expected to be over by July 2023; interest rates likely to drop from mid-2024

The gradual economic improvement seen in recent months has hit a minor obstacle. "The UniCredit Bank Austria Business Indicator fell to minus 1.6 points in March, marking a low for the year to date. The economic outlook had been looking brighter since the start of the year, but progress is now being hampered by dark clouds gathering on the horizon in the domestic industrial sector and some service sectors", says UniCredit Bank Austria Chief Economist Stefan Bruckbauer, adding: "The anticipated recovery of the domestic economy has not been sidelined altogether, but we believe it will now be delayed. We are likely to see the first shoots of spring in Q2, with the Austrian economy slowly returning to growth."

Achieving an average of minus 1.3 points in Q1 2023, the UniCredit Bank Austria Business Indicator points to a slight decline in economic performance in Austria at the start of 2023. "Following a period of stagnation at the end of 2022, we expect GDP to decline slightly for the first three months of this year when compared to the previous quarter. Weak consumer demand as a result of high inflation has severely limited performance in many services sectors — retail in particular. The global economy has not been in a position to prop up performance either, leading to weaker export figures and weighing on the industrial sector. These conditions have had a noticeable impact on investment activity — particularly given the sizeable decline in new orders in the construction sector", says Bruckbauer.

Deterioration in certain services sectors, particularly retail and hospitality and accommodation, dragging down economic mood

Worsening sentiment in the services sector was the biggest driver of the decline in the UniCredit Bank Austria Business Indicator in March. The business outlook dipped for the first time in four months, falling below the long-term average. Accommodation and hospitality services in particular, along with retail, are likely to see price increases dampen demand in the interim. Consumer sentiment has nonetheless continued its slight upwards trend despite high inflation and the real-terms loss of income for many sectors of the population, although the mood has remained strongly pessimistic since the outbreak of war in Ukraine.

The decline in sentiment in the domestic industrial sector also contributed to the drop in the UniCredit Bank Austria Business Indicator, despite the global export environment beginning to improve again. The negative impact from Germany was offset by the positive performance in Eastern Europe and other areas. Improvements with the supply chain problems and falling commodity prices have nonetheless driven only a slight improvement in the indicator that monitors the global mood in the industrial sector (and is weighted by the Austrian share of trade). Declines in demand in industries such as plastics, electricals, paper and mechanical engineering, on the other hand, had a negative impact on sentiment in the domestic industrial sector.

By contrast, the slump in sentiment eased off in the construction sector. While unfavourable trends in structural engineering continued, driven by the reduced affordability of residential properties due both to prices and to new lending arrangements and rising interest rates, the civil engineering sector was responsible for a slight improvement in economic momentum in the construction sector as a result of public projects.

Delayed does not mean lost

The global economic outlook has improved in recent months, although the positive effects of the Chinese economy opening back up following another wave of the COVID-19 pandemic have so far been more limited than expected. Nevertheless, the export economy points to a noticeable revival of the domestic economy over the coming months. The export-oriented industrial sector will benefit from growth in demand from abroad, leading investment activity to gradually regain momentum over the course of the year.

Consumption will once again become a growth pillar as inflation gradually reduces. Stable development on the labour market and real-terms income growth from H2 onwards will trigger rising demand in the retail and hotel and restaurant sectors. "The expected recovery has been slow to materialise. Based on the revival of the export economy, however, the Austrian economy is set to gain greater momentum in the coming months. While investment activity will remain sluggish due to the changed financing conditions—particularly in the construction sector—the decline in inflation is expected to boost consumption", says UniCredit Bank Austria Economist Walter Pudschedl, adding: "Following a weak start to the year and an initially hesitant recovery, we continue to expect only moderate economic growth of 0.7% for 2023 as a whole. For 2024, we expect a slight recovery at 1.2%."

"Despite the current economic slowdown and the pace of recovery remaining only moderate, the domestic labour market will remain extremely robust. The average unemployment rate for 2023 is expected to increase slightly to 6.4% before declining to 6.3% or lower in 2024", says Pudschedl.

Inflation beginning to decline

Inflation began to reduce in Austria as the year progressed. In March, the fall in energy prices and certain administrative measures such as the electricity price brake saw inflation fall to single digits for the first time in six months, at an estimated 9.1%. While the downwards trend in overall inflation is expected to continue, core inflation, i.e. inflation excluding energy and unprocessed foodstuffs, has not yet peaked. It is even expected to have exceeded total inflation in March.

"Rising wage costs will continue to generate upwards movement in services prices for some time to come and will delay the decline in overall inflation, due to the further weakening price pressure for goods", says Pudschedl, adding: "We expect inflation to fall to 6.5% on average for 2023, but with a clear risk of it rising. This means that the inflation rate in Austria will be noticeably higher than the rate of 5.5% in the eurozone, due to strong second-round effects. We expect inflation of 3.0% in 2024, which remains higher than the anticipated figure of 2.4% for the eurozone."

Rate hikes nearing an end

In the face of continued increases in core inflation, the European Central Bank is sticking to its tight monetary policy course for the time being. However, recent turmoil on the markets is likely to accelerate the transfer of monetary policy, reducing the need for further rate hikes.

"We have reduced our expectations for both the deposit and refinancing rates by 25 basis points. We now anticipate a further three increases of 25 basis points each in May, June and July this year. This would take the deposit rate to a maximum of 3.75% and the refinancing rate to a maximum of 4.25%", says Bruckbauer.

"The cycle of monetary tightening is nearing its end. However, the ECB will only react after a significant slowdown in core inflation. We do not expect interest rate cuts of 75 basis points in the eurozone until mid-2024", concludes Bruckbauer.

Enquiries:

UniCredit Bank Austria Economics & Market Analysis Austria

Walter Pudschedl, Tel.: +43 (0)5 05 05-41957;

Email: walter.pudschedl@unicreditgroup.at